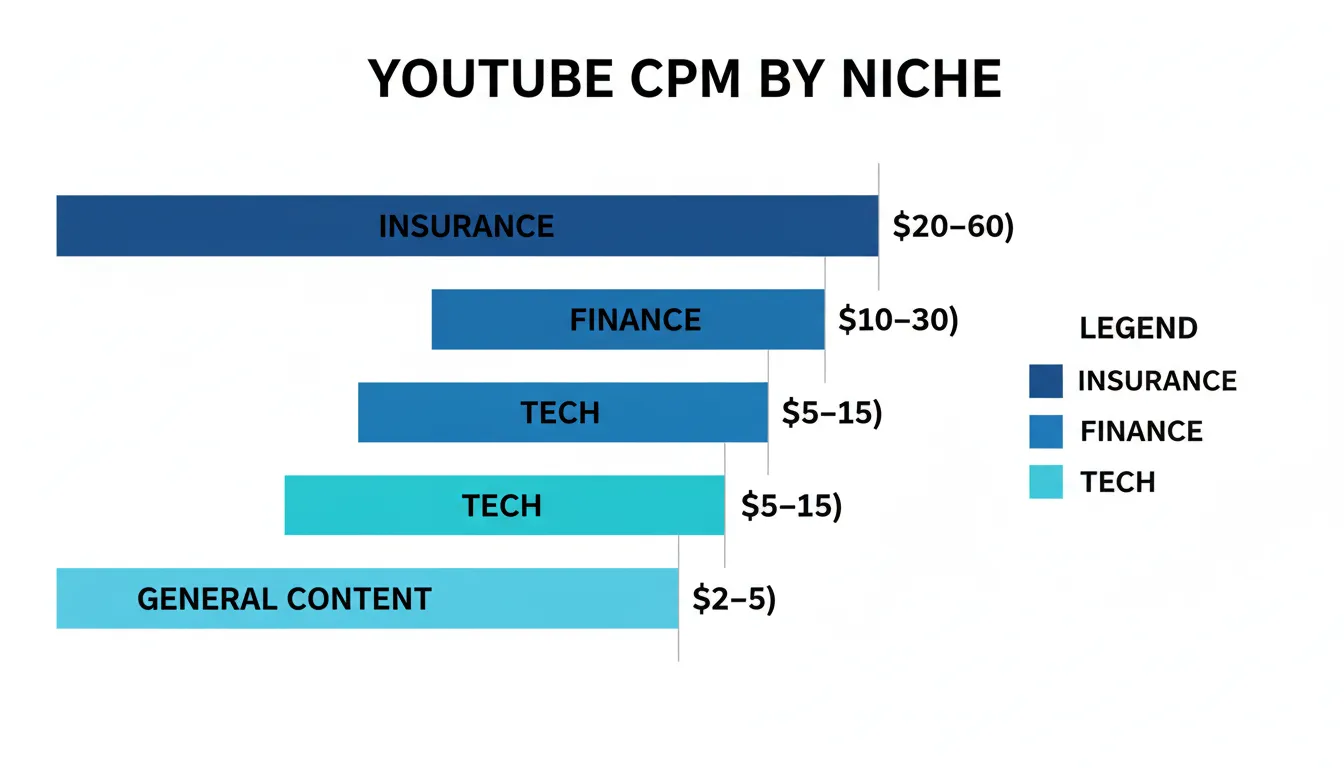

If you’re a content creator grinding on YouTube and making less than $10 per 1,000 views, you’re leaving serious money on the table. While the average YouTuber earns $2–$5 CPM (cost per thousand impressions), creators in the insurance niche are pulling in $20–$60+ CPM. That’s not a coincidence. It’s by design. Insurance keywords are the most expensive on the internet because advertisers—primarily financial services companies—are willing to pay premium prices to reach qualified audiences. In 2026, the insurance niche isn’t just profitable. It’s the single highest-paying category on YouTube for creators willing to specialize. This comprehensive guide reveals exactly why, how much you can realistically earn, and the specific strategies top insurance creators use to maximize RPM (revenue per thousand impressions) year-round.

What Is YouTube RPM and Why Insurance Dominates

YouTube RPM (Revenue Per Mille) is the amount you earn per 1,000 views after YouTube takes its 45% cut and accounting for factors like geography, viewer engagement, and ad demand. It’s different from CPM, which is what advertisers pay. If a CPM is $40, your RPM might be $18–$22 after platform fees and payment processing. Understanding this distinction is critical because insurance niche RPM rates are genuinely exceptional—not just in absolute numbers, but compared to every other content category on the platform.

Insurance dominates because of advertiser demand and audience intent. When someone searches “best life insurance for seniors” or “term vs whole life insurance comparison,” they’re displaying purchase intent. They’re likely in a decision-making phase. Insurance companies and brokers will pay $30–$60 per click for that traffic because it converts. Compare this to fitness content (CPM: $8–$12) or general entertainment (CPM: $1–$3). The difference isn’t marginal. It’s transformative to your income. A creator with 100,000 monthly views in fitness earns roughly $800–$1,200. The same creator with 100,000 views in insurance earns $2,000–$6,000. That’s a 2–6x income multiplier for the exact same effort—just a different niche focus.

The insurance landscape in 2026 is particularly lucrative because of several converging trends. First, an aging population means more people seeking retirement and healthcare solutions. Second, regulatory changes in insurance advertising (especially around annuities and long-term care) have made compliant educational content more valuable. Third, YouTube’s algorithm increasingly favors expert content in YMYL (Your Money, Your Life) categories—which includes insurance. Advertisers trust YouTube insurance creators because they’re addressing genuine audience pain points.

The Real Numbers: Insurance CPM and RPM Breakdown by Sub-Niche

Not all insurance content pays equally. The insurance niche breaks down into specific sub-categories, each with distinct CPM and RPM ranges. Understanding this breakdown is essential for strategic channel positioning.

Life Insurance: $20–$60 CPM / $10–$28 RPM. This is the bread and butter of insurance YouTube. Life insurance requires personalized recommendations, making it perfect for educational content. Term life, whole life, universal life, and indexed universal life (IUL) all attract high-CPM ads because commissions in the life insurance space are substantial ($500–$5,000+ per policy).

Health Insurance: $15–$45 CPM / $7–$21 RPM. This includes Medicare Advantage, Medigap, ACA marketplace content, and employer health plan reviews. It’s slightly lower than life insurance because health insurance buyers are often searching for information rather than immediate purchase intent.

Auto Insurance: $12–$35 CPM / $6–$16 RPM. While still excellent, auto insurance CPM is lower than life or health because the average policy value is smaller. However, volume can compensate—auto insurance is extremely searchable content.

Annuity and Retirement Planning: $35–$70+ CPM / $16–$32+ RPM. This is the absolute premium tier. Annuity commissions are massive (sometimes 6–10% of the policy value), and advertisers will pay accordingly. Annuity comparison videos, fixed indexed annuity reviews, and retirement income strategy content attract the highest-paying ads on YouTube.

Home and Renters Insurance: $10–$30 CPM / $5–$14 RPM. Lower than life or health insurance but still significantly above general content. Homeowner insurance content gets steady search volume with good intent signals.

Disability and Long-Term Care Insurance: $25–$55 CPM / $12–$26 RPM. These policies have high individual premiums and are often recommended by financial advisors. The CPM reflects the value advertisers place on reaching people considering these products.

A real-world example: A YouTube channel called “Retirement Clarity” focused exclusively on Medicare and annuity comparisons. In their first year, they achieved a $24 average RPM. By year two, after refining their audience targeting and content strategy, they hit $31 RPM. With 500,000 monthly views, that’s the difference between $12,000 and $15,500 in monthly earnings—just from optimizing niche positioning.

How to Position Your Channel for Maximum Insurance CPM

Simply creating insurance content isn’t enough. Smart positioning maximizes your CPM and attracts the highest-paying advertisers. Here’s the strategic framework top creators use.

1. Choose Your Sub-Niche (Don’t Be Generalist)

Creators who make the most money don’t cover “insurance broadly.” They specialize. A channel that does only Medicare Advantage content will earn more CPM than a channel jumping between car insurance, home insurance, and health insurance. Why? Because advertisers bid specifically for audiences. A Medicare Advantage insurance company doesn’t want their ads on auto insurance content—it’s wasted spend. When you specialize, YouTube’s algorithm matches your content with higher-paying ads specifically designed for that audience.

Recommendation: Pick one of these sub-niches and build around it:

– Medicare and supplemental insurance (excellent for 50+ demographic)

– Life insurance for families (broad, searchable, high CPM)

– Annuities and retirement income (highest CPM, smaller audience)

– Business insurance for small business owners (niche, high-value)

2. Build Authority and E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness)

Google and YouTube’s algorithm prioritize E-E-A-T, especially for YMYL content. This means:

– Display credentials (insurance licenses, financial certifications)

– Cite regulatory sources (SEC, NAIC, Medicare.gov)

– Reference academic research and actuarial data

– Show years of experience or client testimonials

A channel with “Insurance Agent Reviews” won’t outcompete a channel run by a licensed insurance agent with 15 years of industry experience. Advertisers know this. They’ll pay higher CPM for content from verified experts because it converts better. If you don’t have direct credentials, partner with someone who does—or build credibility through consistent, accurate content over time.

3. Target High-Intent Keywords

Not all insurance keywords are equal. Some attract $5 CPM. Others attract $50+ CPM. The difference is search intent and advertiser value.

High-CPM keywords:

– “Best annuity rates” ($45–$70 CPM)

– “Medicare Advantage vs Medigap” ($35–$55 CPM)

– “Whole life insurance worth it” ($25–$45 CPM)

– “Best life insurance for seniors with health problems” ($30–$50 CPM)

– “Fixed indexed annuity reviews” ($40–$65 CPM)

Lower-CPM keywords (but still solid):

– “How much life insurance do I need” ($15–$25 CPM)

– “Term life insurance explanation” ($12–$22 CPM)

– “Affordable car insurance” ($8–$18 CPM)

Your content strategy should weight heavily toward high-intent, comparison-based content. “Top 5 Life Insurance Companies” videos attract higher-CPM ads than “What is term life insurance?” videos—even though the latter gets more views. Prioritize CPM over raw view count.

4. Optimize for Geographic CPM Differences

YouTube CPM varies dramatically by viewer location. Creators with predominantly US audiences earn $3–$4x more than creators with predominantly African or Southeast Asian audiences. This is simply how advertiser demand works.

While you can’t prevent viewers from other countries, you can strategically position your content for high-CPM regions:

| Region | Insurance CPM Range | Strategy |

| ——– | ——————- | ———- | <br /> |

|---|---|---|---|

| USA | $20–$70 | Primary target. Advertiser volume is highest. | |

| Canada | $12–$40 | Secondary target. Strong insurance market. | |

| UK | $10–$35 | Growing market for financial content. | |

| Australia | $8–$30 | Good CPM, English-speaking audience. | |

| India | $2–$8 | Large audience, low CPM. Lower priority. |

If your analytics show significant international traffic, use titles and thumbnails that appeal specifically to US/Canada/UK audiences. “Best Life Insurance for Americans” outperforms “Best Life Insurance Worldwide.” This subtle positioning shift can lift your overall RPM by 15–25%.

5. Create Comparison and Review Content (Not Just Educational)

Educational content (“What is whole life insurance?”) converts views but attracts moderate CPM. Comparison content (“Whole life vs universal life vs term life”) attracts premium CPM because it signals purchase intent.

The highest-paying content format: structured comparison videos.

Example structure:

– Policy 1: Pros, cons, price, best for

– Policy 2: Pros, cons, price, best for

– Policy 3: Pros, cons, price, best for

– Side-by-side comparison table

– Conclusion with recommendation framework

This format attracts ads from competing insurance providers bidding for the same audience. Multiple advertisers bidding = higher CPM. A side-by-side comparison video gets 30–50% higher CPM than a single-product explainer.

Key Takeaways

Tools, Resources, and Infrastructure for Insurance Content Success

Creating consistent, high-quality insurance content requires specific tools and infrastructure. Here’s what working insurance creators use.

Content Research and SEO

– Ahrefs ($99–$399/month): Track keyword difficulty, search volume, and competitor content. Identify high-CPM insurance keywords.

– TubeBuddy ($9–$49/month): YouTube-specific research showing estimated revenue per video and keyword opportunity scoring.

– Google Trends: Free tool for identifying emerging insurance topics and seasonal trends (e.g., “Medicare enrollment” spikes Oct-Dec).

– Answer the Public ($99/month or free limited version): Shows questions people actually ask about insurance topics—perfect for video ideas.

Content Production

– Descript ($12–$24/month): AI-powered video editing. Perfect for insurance content creators who want professional results without complex editing.

– Camtasia ($99 one-time): Screen recording and editing for insurance product walkthroughs and comparison demonstrations.

– Canva Pro ($120/year): Create professional insurance comparison charts, infographics, and slides for B-roll.

Analytics and Revenue Optimization

– YouTube Analytics: Free but requires daily monitoring. Track CPM trends, audience demographics, and click-through rates on ads.

– Google AdSense: Monitor which specific insurance ad types earn highest CPM on your channel.

– Social Blade ($5–$20/month): Project revenue and track RPM growth over time.

Compliance and Regulatory

– Insurance regulatory databases (SEC EDGAR, NAIC database): Free but requires navigation. Essential for citing accurate information.

– Medicare.gov: Free source for Medicare and Medigap data. Bookmark this.

– Zoom ($16–$31/month): Record interviews with insurance professionals to add credibility and authority to content.

Estimated Monthly Tool Cost: $150–$400 depending on which combination you choose. This investment is recouped quickly in a niche earning $20–$60 CPM.

Pros and Cons of the Insurance Niche on YouTube

Pros:

✓ Exceptional CPM rates: $20–$70 CPM is 5–10x higher than general content, directly translating to higher RPM and revenue.

✓ Consistent ad demand: Insurance companies and brokers advertise year-round because insurance needs never stop. Unlike seasonal niches (holiday content, back-to-school), insurance has steady demand.

✓ Searchable content longevity: Insurance comparison videos remain relevant for 2–3 years. Unlike news or trend content that expires in weeks, insurance videos compound in value.

✓ Algorithm favorability: YouTube’s algorithm rewards E-E-A-T content in YMYL categories. Insurance content benefits from algorithmic prioritization when well-executed.

✓ Diversified monetization: Beyond AdSense, insurance creators earn through affiliate commissions, sponsored content from insurance brokers, and lead generation deals ($5–$25 per qualified lead).

✓ Lower competition than you’d expect: While insurance is valuable, fewer creators specialize in it compared to fitness, finance general, or gaming. Less saturation means easier audience growth.

Cons:

✗ High barrier to entry: Creating credible insurance content requires research, accuracy, and often credentials. You can’t succeed with surface-level knowledge.

✗ Regulatory complexity: Insurance is heavily regulated. Misinformation can result in copyright strikes, demonetization, or legal issues if you misrepresent products.

✗ Slower audience growth initially: Insurance content appeals to a specific demographic (often 40+). Your initial audience grows slower than trending content, requiring patience and consistency.

✗ Smaller absolute audience: A successful insurance channel might reach 50,000–200,000 subscribers. Compare to fitness channels with 500,000+ subscribers. You’re building a smaller but more profitable audience.

✗ Advertiser vetting: Not all insurance companies want YouTube placement. Some are reluctant about third-party reviews. Advertiser volume is high, but selection is curated.

✗ Topic narrowness: Deviation from insurance kills CPM. A video about “insurance and cryptocurrency” or “insurance tips for freelancers” will earn half the CPM because it dilutes your audience targeting.

Net Assessment: The pros far outweigh the cons for creators willing to specialize and invest in accuracy. The income multiplier (5–10x higher than general content) justifies the slower growth and higher barrier to entry.

Real-World Case Studies: Insurance Creators Earning $5,000–$15,000+ Monthly

Case Study 1: “Medicare Secrets” Channel

Profile: Run by a retired healthcare administrator with 12 years in insurance compliance. 85,000 subscribers. 90% US audience, age 50+.

Content Strategy: Weekly Medicare Advantage vs Medigap comparison videos, annual open enrollment guides, Supplemental insurance reviews.

Results (Year 1):

– 150,000 monthly views

– $28 average RPM

– $4,200/month from AdSense

– $1,800/month from insurance broker affiliate commissions

– Total: $6,000/month

By Year 2 (after optimization):

– 280,000 monthly views

– $34 average RPM

– $9,520/month from AdSense

– $2,400/month from affiliates

– Total: $11,920/month

Key factor: Switching from educational content (“What is Medicare?”) to comparison-heavy content (“Medicare Advantage Plans Compared for 2026”). This single shift increased RPM from $18 to $34

Advertisement