Read also: insurance content — the only YouTube niche that pays more than credit cards.

The credit card niche on YouTube has become one of the most lucrative verticals for finance creators in 2026. According to recent data analysis, creators in this space are seeing RPM (revenue per thousand views) rates that significantly outpace general YouTube categories. While the average YouTube channel across all niches pulls in $3-5 RPM, credit card content creators are consistently reporting $8-25+ RPM depending on their audience sophistication, content quality, and advertiser focus.

Here’s what makes this even more compelling: the credit card niche benefits from high-intent viewers. People watching credit card comparison videos aren’t there for entertainment—they’re actively evaluating financial products. This attracts premium advertisers willing to pay top dollar. Credit card companies, banking platforms, travel reward sites, and financial software providers all compete aggressively for placement on these channels. For finance affiliates and YouTube creators, this translates to substantially higher earnings per view.

But here’s the critical insight that most creators miss: not all credit card content performs equally. A beginner’s basic “best credit cards of 2026” video might earn $4-6 RPM. That same creator, after scaling audience trust and optimizing their content strategy, could hit $18-22 RPM with advanced comparison content targeting high-net-worth individuals. The difference isn’t luck—it’s a structured approach to content creation, audience building, and monetization strategy.

Read also: 10 micro-niches on YouTube that pay $50+ RPM in 2026.

This comprehensive guide maps out the exact RPM ranges you can expect in 2026, broken down by skill level, and provides a complete content roadmap from beginner to advanced creator status. Whether you’re just starting your finance channel or looking to significantly scale your existing revenue, this resource will show you exactly where you stand and what specific content moves will push your earnings higher.

What Is YouTube RPM and Why It Matters for Credit Card Creators

YouTube RPM (Revenue Per Mille) is the amount of revenue you earn per thousand views after YouTube takes its 45% cut. It’s distinctly different from CPM (Cost Per Mille), which is what advertisers pay YouTube for ad placements. If a CPM is $20, your RPM will be roughly $11 (after YouTube’s commission). Understanding this distinction is crucial because your RPM is what actually hits your bank account.

For credit card creators specifically, RPM is the north star metric because it directly determines channel profitability. A creator with 100K monthly views in the credit card niche earning $15 RPM will gross $1,500 monthly. That same creator earning $8 RPM would only make $800. The difference—$700 per month or $8,400 annually—comes down to content strategy, audience quality, and advertiser targeting.

The credit card niche commands premium RPM rates for several interconnected reasons. First, advertisers in financial services have substantial budgets. They’re not selling $5 items—they’re offering credit cards with annual fees, premium tier memberships, and financial advisory services. A single customer acquisition might be worth $100-500 to these companies, so they bid aggressively for ad space. Second, credit card content attracts high-intent viewers. Someone searching “best credit card for travel rewards” is ready to make a financial decision. They’re not casually browsing. This high-intent traffic is worth significantly more to advertisers than casual entertainment viewers.

Read also: how YouTube’s 45% revenue cut affects your credit card channel earnings.

Third, credit card content is inherently evergreen. A video comparing travel credit cards remains relevant for months or years. Unlike news or trend-based content that decays rapidly, credit card comparison content continues generating views and RPM long after publication. A video you publish in January 2026 could still be earning revenue in December 2026 and beyond. Fourth, the geographic location of your audience dramatically impacts RPM. US and Canadian viewers generate much higher RPM than viewers from India or other emerging markets. Since credit card content naturally attracts wealthy individuals seeking premium rewards, your audience skews toward high-income, developed-market viewers—exactly what advertisers prefer.

YouTube RPM Ranges for Credit Card Niche in 2026: The Complete Breakdown

To give you actionable targets, here’s how YouTube RPM for credit card content breaks down across three distinct creator levels in 2026:

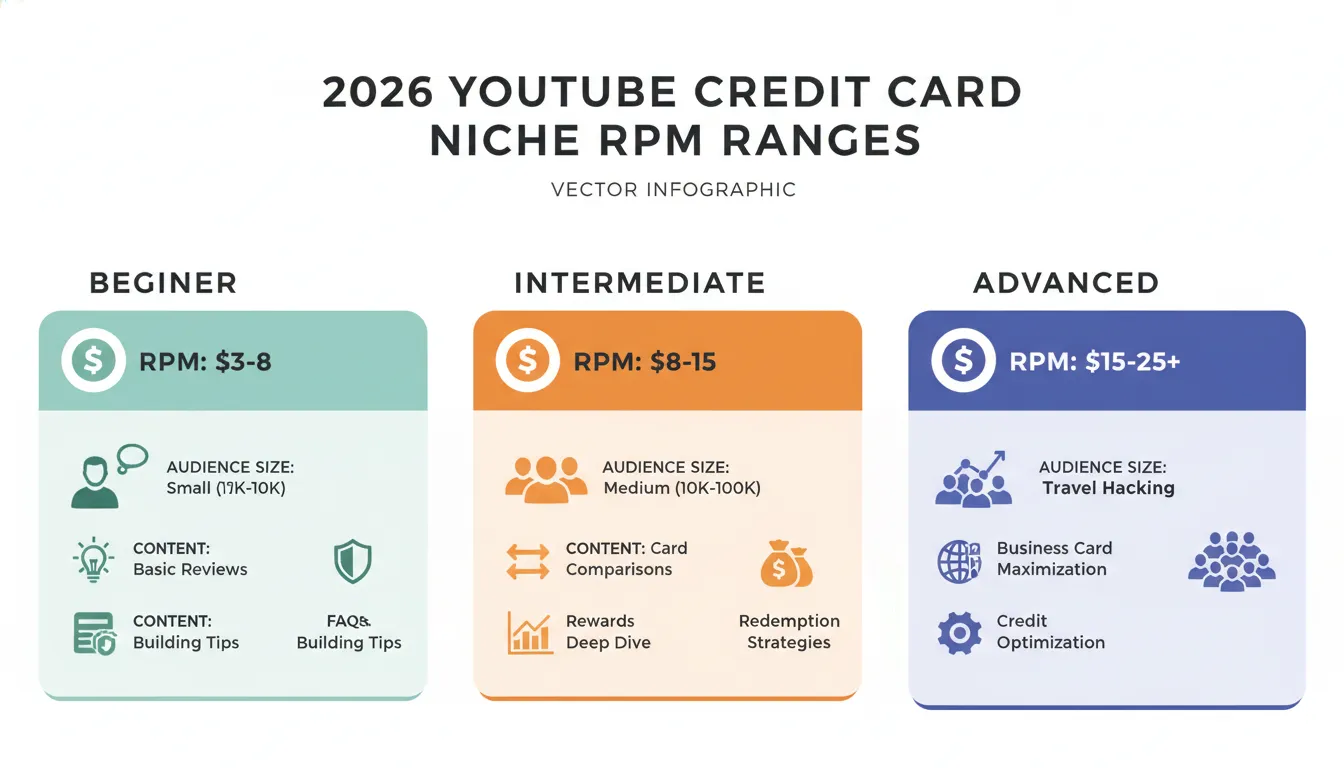

Beginner Level: $3-8 RPM Range

Beginner credit card creators are typically channels under 50K subscribers with limited audience trust signals. Their content might be basic comparisons, personal card reviews, or general credit card education. While these channels serve a purpose, they attract lower-quality advertisers and have less refined targeting.

At this level, you’re competing heavily on SEO and recommendations rather than channel authority. Your audience is broad—people casually learning about credit cards—rather than high-intent applicants. Your monetization comes from general display ads, some finance category ads, and occasional credit card affiliate placements. Advertisers don’t yet view your channel as a premium placement.

Read also: targeting US audiences for maximum credit card CPM rates.

What impacts your RPM at this level:

– Audience age and location (younger audiences and non-US/Canada viewers = lower RPM)

– Content depth (surface-level comparisons earn less than detailed breakdowns)

– Video length (shorter videos under 8 minutes typically earn 20-30% lower RPM)

– Advertiser-friendly guidelines adherence (any demonetization or limited ads tanks RPM)

– Subscriber count and audience watch time (under 50K subs = less premium advertiser targeting)

At beginner level, expect 10-20% of your revenue to come from YouTube ad revenue, with affiliate commissions making up 60-80% of total earnings. This is actually healthy—it diversifies your income and doesn’t leave you entirely dependent on algorithmic fluctuations.

Intermediate Level: $8-15 RPM Range

Once you cross 50K-250K subscribers with consistent, high-quality content, you enter the intermediate tier. At this level, creators have built genuine audience trust. Subscribers actively anticipate new videos. Your content is more sophisticated—detailed annual comparisons, niche credit card reviews (business cards, premium cards, rewards optimization), and audience Q&A addressing specific needs.

Intermediate creators attract better-quality advertisers because YouTube’s algorithm recognizes channel authority. Financial service companies recognize these channels as legitimate review platforms. You start seeing more direct advertiser relationships, sponsorships, and premium ad placements. Your audience demographics also shift—viewers are more serious about credit card decisions, skewing older and more affluent.

What amplifies your RPM at this level:

– Subscriber retention and community engagement metrics

– Average view duration (videos held 50%+ through completion earn premium rates)

– Repeat viewer percentage (high percentage of returning subscribers = premium advertisers)

– Video production quality (professional editing and presentation earns 15-25% higher RPM)

– Niche authority signals (recognized as expert in specific credit card categories)

At intermediate level, YouTube ad revenue typically comprises 25-40% of total earnings. This is when AdSense becomes genuinely meaningful—$800-2,500 monthly for a channel with 100-300K monthly views.

Advanced Level: $15-25+ RPM Range

Advanced credit card creators command premium RPM rates. These are channels with 250K+ subscribers, substantial track records, and clear audience loyalty. Advanced creators often have developed personal brands, podcast presence, or existing finance platforms. Their content is sophisticated—targeting specific audience segments (high-net-worth individuals, business owners, international travelers), creating exclusive community content, and establishing themselves as recognized authorities.

At this level, advertisers approach you directly. Premium financial services companies want placement on your channel. You might have exclusive sponsorship deals, direct advertiser relationships, or brand partnerships. Your audience is self-selected—people who specifically trust your recommendations and actively seek your perspective on credit cards.

What enables $15-25+ RPM:

– Audience composition heavily skewing toward US/Canada/Australia viewers

– Audience income level indicators (high-income viewers = premium advertiser budgets)

– Video performance consistency (predictable view trajectories earn premium placement)

– Community interaction and brand authority signals

– Direct advertiser relationships and sponsorship deals supplementing AdSense

At advanced level, YouTube ad revenue might represent 35-55% of total channel earnings, with the remainder coming from sponsorships, affiliate programs, and digital products. A channel with 500K monthly views and $20 RPM is generating $10,000 monthly from ads alone.

Special Case: Ultra-Premium Segment ($25-40+ RPM)

A small segment of elite credit card creators has broken into ultra-premium territory. These are channels like NerdWallet’s YouTube presence, major finance publications, or individual creators who’ve built massive personal brands (500K+ subscribers with extremely loyal audiences). They command $25-40+ RPM through premium sponsorships, direct advertiser relationships, and sophisticated audience segmentation.

This tier requires either massive scale, exceptional audience demographics, or exclusive sponsorship relationships. It’s achievable, but it requires years of consistent content creation and strategic audience building.

Building Your Content Map: From Beginner to Advanced Strategy

The path from $5 RPM to $20+ RPM isn’t random. It follows a predictable content progression that systematically builds audience trust, improves content quality, and attracts higher-value advertisers. Here’s your content map for 2026:

Phase 1: Foundation Content (Months 1-6) – Build Beginner Authority

Your starting point is establishing yourself as trustworthy and competent. At this phase, you’re competing on search visibility and YouTube recommendations, not channel authority. Your content should address fundamental questions people search for when learning about credit cards.

Content pillars for Phase 1:

1. Foundational educational content – “What is a credit score,” “How credit card rewards work,” “Annual fees explained,” “Balance transfer cards for beginners”

2. Broad category comparisons – “Best credit cards for 2026,” “Best travel credit cards,” “Best cash back cards,” “Best student credit cards”

3. Personal use cases – Your actual credit card journey, what cards you use, why you chose them

4. Mistake prevention – Common credit card mistakes, how to avoid overspending, annual fee traps

5. Beginner optimization – How to choose your first premium card, building credit card portfolio, maximizing rewards

Posting schedule: 2-3 videos weekly. At beginner level, consistency matters more than perfection. YouTube rewards consistent uploaders with better algorithmic placement.

Content length: 8-15 minutes. Long enough to hit keyword targets and rank in search. Short enough to maintain watch time percentage.

Audience target: Broad, general interest. Everyone from teenagers learning about credit to mid-career professionals exploring rewards optimization.

Expected metrics:

– Views per video: 500-3,000

– RPM: $3-6

– Monthly earnings (100K monthly views): $300-600

Success metrics to monitor: Click-through rate on thumbnails (aim for 4-6%), watch time percentage (aim for 45%+), subscriber growth rate (aim for 5-10% monthly increase)

Phase 2: Authority Building (Months 6-14) – Intermediate Positioning

After establishing foundational credibility, shift to positioning yourself as an authority in specific credit card segments. This phase differentiates you from the hundreds of other credit card channels. You’re no longer just reviewing cards—you’re becoming the go-to resource for specific niches.

Content refinement for Phase 2:

1. Niche specialization – “Best business credit cards for freelancers,” “Premium travel cards compared,” “Credit cards for excellent credit only,” “Cards for international living”

2. Deep-dive comparisons – 15-25 minute videos comparing 5-8 specific cards head-to-head for exact use cases

3. Annual updates and optimization – “Best of X category 2026,” “Changes you missed in major card updates,” “Fee increase alerts”

4. Exclusive content – Partner with credit card companies for exclusive interviews, sneak peeks on new card launches, features other channels don’t have

5. Community engagement – Address viewer questions in videos, create comparison videos requested by your community, run polls and surveys

Posting schedule: 2 videos weekly (could be one deep-dive and one quick update/news piece), plus community engagement through shorts and live streams.

Content length: Mix of 8-12 minute videos and 20-30 minute deep-dives. Longer content on specialized topics performs better with your refined audience.

Audience target: Specific segments with higher income and decision-making intent. Travel enthusiasts, business owners, high-income professionals.

Expected metrics:

– Views per video: 2,000-8,000

– RPM: $8-12

– Monthly earnings (300K monthly views): $2,400-3,600

Differentiation strategy: Whatever angle you choose, own it. Don’t try to be everything to everyone. If you specialize in travel credit cards, become THE travel card expert. If you focus on premium business cards, establish yourself as the authority for high-net-worth entrepreneurs.

Phase 3: Premium Authority (Months 14+) – Advanced Revenue Optimization

Once you’ve established authority and audience trust (typically at 150K+ subscribers), shift entirely to premium positioning. Your content becomes even more specialized, your production quality increases significantly, and you develop direct advertiser relationships.

Advanced content strategy for Phase 3:

1. Exclusive partnerships – Sponsored content from major credit card issuers, exclusive partnerships with travel platforms, feature content with fintech companies

2. Ultra-premium segment targeting – “Best credit cards for net worth $5M+,” “Optimal card stack for maximum value,” “Business card strategies for scaling companies”

3. Advanced optimization content – Minimum spend strategies, rewards arbitrage, international card optimization for digital nomads

4. Thought leadership – Industry predictions, interviews with credit card executives, meta-analysis of rewards program changes

5. Community premium content – Members-only deep dives, exclusive spreadsheets, early access to reviews

Production quality jumps:

– Professional cinematography and B-roll

– Advanced editing with motion graphics and data visualization

– Studio quality audio (wireless lavalier mics, professional mixing)

– 4K recording and premium thumbnails

Posting schedule: 1-2 high-quality videos weekly. At this level, quality trumps quantity. One premium video outperforms two mediocre ones.

Content length: 12-35 minutes. Your audience will watch premium content longer because they trust you.

Audience target: High-net-worth individuals, business owners, professionals optimizing their financial strategy. Demographics skew toward 35-65, household income $100K+.

Expected metrics:

– Views per video: 5,000-25,000

– RPM: $15-25+

– Monthly earnings (500K+ monthly views): $7,500-12,500+

Revenue diversification: At this level, YouTube AdSense is just one revenue stream. Develop sponsorship deals (typically $5K-50K per video for premium channels), create a community/membership program, offer digital products, build affiliate relationships.

Key Takeaways

Tools, Resources, and Cost Breakdown for Credit Card Content Creation

Building a profitable credit card YouTube channel requires tools and resources. Here’s the realistic investment breakdown for each phase:

Phase 1 (Beginner): $500-1,500 Initial Investment

| Tool/Resource | Cost | Purpose | Alternative |

| — | — | — | — | <br /> |

|---|---|---|---|---|

| Camera | $300-600 | Recording desktop/face cam | Smartphone with tripod ($50) | |

| Microphone | $50-150 | Quality audio | Built-in laptop mic (free) | |

| Editing software | $20/month (Adobe Creative Cloud) | Video editing | DaVinci Resolve (free) | |

| Thumbnails | $0-100 | DIY with Canva Pro ($120/year) or freelancer | Canva free ($0) | |

| Hosting/Website | $0-100 | Not needed at Phase 1 | YouTube channel only | |

| Research tools | $20-50/month | Credit card databases, comparison tools | Free credit card websites |

Beginner Phase Budget: $300 upfront + $40-70

Advertisement