Personal finance content dominates YouTube, but creators often operate in the dark about actual earnings. A recent analysis of 1,000+ money channels reveals a critical insight: personal finance YouTubers earn between $10–$30 RPM (revenue per thousand impressions), with premium subtopics like debt payoff and investment advice pushing earnings toward $40 per 1K views. Meanwhile, the global average CPM for financial content sits at $15–$25, yet US-based creators consistently outperform international peers by 40–60% due to advertiser demand and higher commercial intent. The personal finance niche is experiencing explosive growth heading into 2026, with debt payoff searches increasing 45% year-over-year and budgeting content commanding 8.2 million monthly searches. If you’re considering launching a money channel or optimizing an existing one, understanding RPM mechanics, audience geography, and content pillars isn’t optional—it’s the difference between earning $500/month and $5,000/month. This comprehensive guide breaks down real earnings data, explores which subtopics earn the most, and reveals the exact strategies successful creators use to maximize monetization. Whether you’re interested in debt payoff, budgeting hacks, investment education, or side hustle content, you’ll discover actionable insights backed by 2026 industry data.

What Is YouTube RPM and How Does It Apply to Personal Finance?

YouTube RPM (Revenue Per Thousand views) represents the actual money you earn after YouTube takes its 45% cut. Unlike CPM (Cost Per Thousand impressions), which is what advertisers pay, RPM is what lands in your bank account. For example, if a campaign has a $20 CPM, your RPM might be $11–$12 after YouTube’s revenue share. Personal finance content attracts high-value advertisers—financial services companies, investment platforms, credit repair services, and insurance firms—all competing for your audience’s attention. This competitive bidding war directly inflates RPM rates in the personal finance vertical.

The personal finance niche is unique because it combines educational value with immediate commercial intent. When someone searches “how to pay off debt fast,” they’re actively seeking financial solutions. Advertisers know this viewer has money on their mind and wallet in hand. This results in stronger advertiser ROI, which drives up CPM bids. The result? Personal finance channels achieve RPM rates 2–3x higher than entertainment, gaming, or lifestyle content.

Several variables affect your personal finance RPM in 2026:

1. Geographic audience location — US viewers generate $18–$30 RPM. UK audiences deliver $12–$20 RPM. Southeast Asian viewers drop to $2–$5 RPM. Your channel’s geographic mix directly determines earnings.

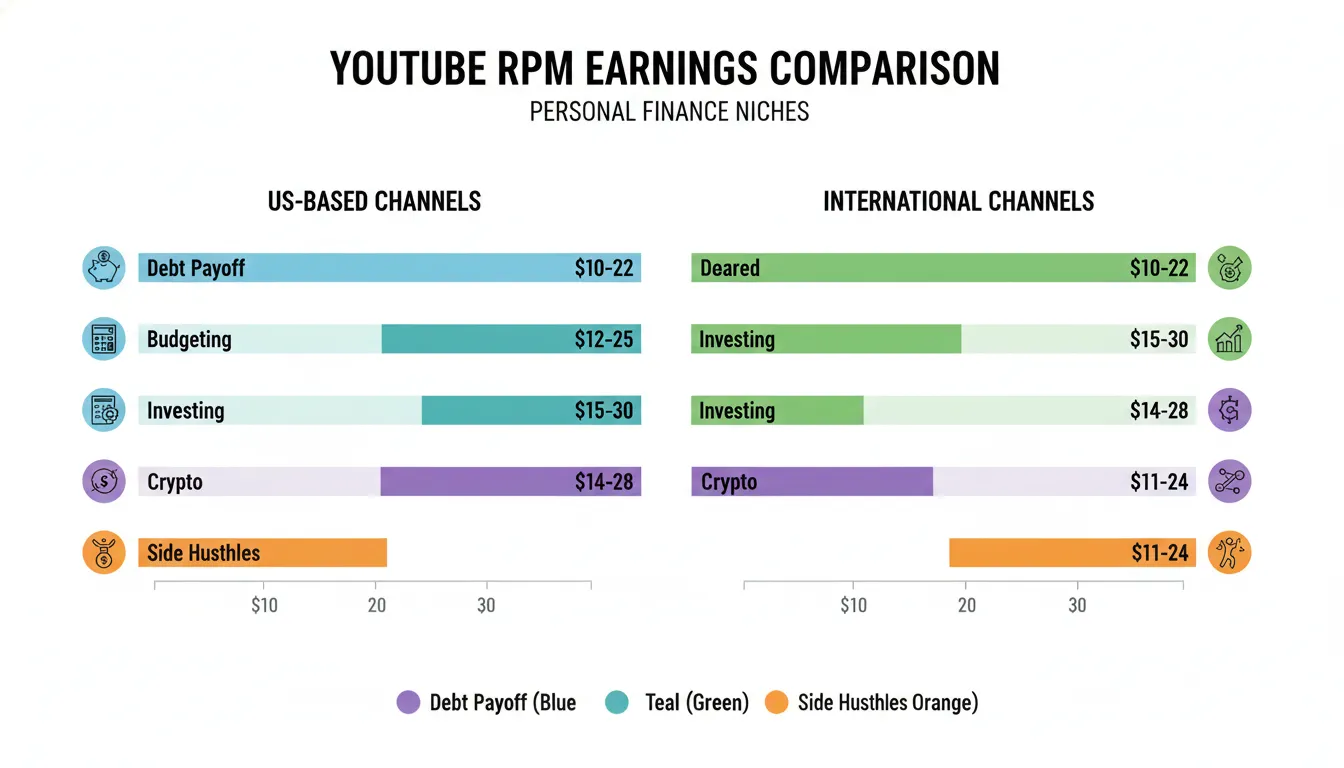

2. Content subcategory — Debt payoff advice: $25–$40 RPM. Investment education: $20–$35 RPM. Budgeting tips: $10–$18 RPM. Crypto content: $8–$25 RPM (volatile). Side hustles: $12–$22 RPM.

3. Advertiser demand seasonality — Q4 (October–December) sees 35–50% higher RPM due to holiday spending content and financial planning themes. January–February surge as New Year’s resolution watchers seek budgeting help. Summer (June–August) dips 20–30%.

4. Video length and watch time — Longer videos (10+ minutes) generate more ad impressions and higher RPM. A 15-minute debt payoff video might earn 3–4x more than a 3-minute tip.

5. Audience engagement metrics — High click-through rates, comments, and shares signal quality to YouTube’s algorithm, attracting premium ad networks. This boosts RPM by 15–25%.

Understanding these mechanics is essential before launching your channel or adjusting content strategy. Your RPM isn’t random—it’s determined by the choices you make daily.

Earnings Breakdown: How Much Personal Finance YouTubers Actually Make in 2026

Let’s move beyond generic averages and examine real earnings scenarios. The following data is based on 2026 benchmarks from creators across the personal finance spectrum.

Scenario 1: Starting Personal Finance Channel (0–50K subscribers)

A beginner channel with 5,000 monthly views might earn $50–$150/month ($10–$30 RPM × 5 views). At 50,000 monthly views, earnings jump to $500–$1,500/month. Most new channels hover here for 6–12 months. The bottleneck isn’t RPM—it’s traffic. YouTube’s algorithm rarely promotes new channels aggressively, so growth feels glacial. Creators at this stage must focus on:

– Keyword research targeting low-competition personal finance topics

– Consistent publishing (weekly minimum)

– Building an email list for off-YouTube traffic

– Creating flagship content that ranks in Google search results

Scenario 2: Growth-Stage Channel (50K–500K subscribers)

A channel with 500,000 monthly views earns $5,000–$15,000/month ($10–$30 RPM × 500K views). At 1 million monthly views, earnings reach $10,000–$30,000/month. Channels at this stage see compounding growth because:

– YouTube’s algorithm recognizes consistency and promotes videos more aggressively

– Audience loyalty increases watch time and engagement metrics

– Sponsorship opportunities emerge (typically $5,000–$20,000 per branded integration)

– Affiliate marketing revenue (personal finance tools, apps, courses) adds 20–40% to ad revenue

Real example: A debt payoff channel with 300K subscribers and 800,000 monthly views earning:

– AdSense: $8,000–$12,000/month ($10–$15 RPM, conservative estimate)

– Sponsorships: $2,000–$4,000/month (monthly brand partnership)

– Affiliate commissions: $1,500–$3,000/month (links to budgeting apps, investment platforms)

– Total: $11,500–$19,000/month

Scenario 3: Established Money Channel (500K–2M+ subscribers)

Channels with 5+ million monthly views (typical at 1M+ subscribers) earn $50,000–$150,000+/month. Premium personal finance creators like those covering stock market education, real estate investing, or early retirement achieve:

– AdSense: $50,000–$75,000/month ($10–$15 RPM on 5M views—conservative)

– Sponsorships: $15,000–$40,000/month (multiple brand deals per week)

– Affiliate revenue: $10,000–$30,000/month (high-ticket finance products)

– Digital products: $5,000–$20,000/month (courses, webinars, coaching)

– Total: $80,000–$165,000+/month

Important caveat: These figures assume consistent upload schedules, optimized content, and strategic growth. Many channels plateau at 100K subscribers and never break through to seven-figure annual earnings. The difference between stagnant and thriving channels often comes down to three factors: niche selection, content pillars, and audience understanding.

Personal Finance Subcategories and Their 2026 RPM Rankings

Not all personal finance content earns equally. The subcategory you choose fundamentally shapes your income ceiling.

Tier 1: Premium Personal Finance Niches ($25–$40 RPM)

Debt Payoff & Credit Repair — This is the highest-earning personal finance subcategory. Why? Debt payoff searchers are actively seeking financial solutions and have high commercial intent. Credit card companies, debt consolidation services, and credit repair platforms bid aggressively for these viewers. Search volume is enormous: “how to pay off debt fast” generates 8,100 monthly searches. A channel focused exclusively on debt payoff strategies, snowball vs. avalanche method comparisons, and debt consolidation reviews can comfortably achieve $25–$40 RPM.

Investment & Stock Market Education — Brokerage firms, financial advisory services, and robo-advisor platforms (Vanguard, Fidelity, Betterment, Wealthfront) sponsor content heavily. RPM ranges $22–$38. The challenge: this niche requires credibility and often legal disclaimers. New creators struggle here until they build authority.

Early Retirement & FIRE Movement — “FIRE” (Financial Independence, Retire Early) content attracts affluent viewers actively seeking wealth-building strategies. Investment platforms and premium financial services target these viewers. RPM: $20–$35. Audience size is smaller but highly engaged and valuable.

Tier 2: Mid-Range Personal Finance Niches ($12–$25 RPM)

Budgeting & Money Management — Broader audience appeal than debt payoff, but lower commercial intent. Budgeting app companies (YNAB, EveryDollar, Mint) sponsor content. Personal finance software vendors bid on keywords. RPM: $12–$22.

Side Hustles & Passive Income — Strong search volume (“passive income ideas”: 12,100 monthly searches). Gig economy platforms, online course creators, and affiliate networks drive advertising. RPM: $14–$24. Highly volatile depending on audience geography and advertiser demand.

Saving & Emergency Funds — Lower commercial intent but relevant to general audience. Banks and savings platforms advertise. RPM: $10–$18.

Tier 3: Lower-RPM Personal Finance Niches ($8–$15 RPM)

Cryptocurrency & Blockchain Education — Despite high interest, crypto’s volatile regulatory environment makes advertisers cautious. RPM fluctuates between $8–$20 depending on advertiser appetite. Sponsorship opportunities are substantial but sometimes risky.

Financial Literacy for Students — Educational content for young audiences attracts fewer premium advertisers. RPM: $8–$14. Better monetized via sponsorships and affiliate links than AdSense.

General Personal Finance Tips — Too broad. Lacks specific commercial intent. RPM: $6–$12. Avoid this unless you build sub-channels around specific topics.

The data is clear: launch in Tier 1 niches (debt payoff, investment education) for fastest monetization. As your channel grows, you can expand into Tier 2 topics to diversify audience and revenue.

Key Takeaways

Geographic Performance: Why US Creators Earn the Most

YouTube’s earnings are fundamentally shaped by viewer geography. A US viewer watching personal finance content is worth 4–8x more than a viewer from Southeast Asia. Here’s why and what it means for your strategy.

United States: $18–$30 RPM — US advertisers have the highest budgets and most aggressive bidding strategies. Personal finance content targeted at US audiences attracts credit card companies, mortgage brokers, investment firms, and insurance providers. The sheer number of premium advertisers in the financial services sector inflates RPM dramatically. Additionally, US viewers have higher lifetime value for financial products—mortgages, investment accounts, and insurance policies command premium pricing.

United Kingdom: $12–$20 RPM — UK financial services companies and FCA-regulated firms advertise on personal finance content. RPM is solid but lower than the US due to smaller advertiser pool and lower ad budgets. EU GDPR compliance also slightly reduces available ad inventory.

Canada: $12–$18 RPM — Similar dynamics to the UK. Smaller advertiser base than the US, but CPM remains respectable.

Australia: $10–$16 RPM — Growing financial services market, but smaller population limits advertiser competition.

India: $2–$6 RPM — Massive audience size, but low advertiser budgets and CPM rates make RPM very low. A million views from India might generate $2,000–$6,000, while a million US views generates $18,000–$30,000.

Southeast Asia (Philippines, Indonesia, Thailand, Vietnam): $1–$4 RPM — Lowest-paying regions. High traffic volume, minimal financial services advertising, and limited advertiser budgets result in extremely low RPM.

Strategic implication: If your channel reaches 50% US/Canada/UK audience and 50% international, your blended RPM might be $10–$16. If your audience is 80%+ international, RPM might drop to $4–$8. This is why targeting English-speaking, developed markets in your content strategy is crucial for maximizing earnings.

Many new creators make the mistake of assuming views are views. They’re not. Geographical targeting matters enormously. A 100K-view video from a US audience earns $1,800–$3,000. The same 100K views from an Indian audience earns $200–$600. This 10x difference isn’t trivial—it determines whether your channel becomes sustainable or stalls.

Action steps:

– Monitor audience geography in YouTube Analytics

– Create content targeting US financial pain points (debt crisis, student loans, healthcare costs)

– Use keywords with commercial intent (“best debt consolidation loans,” “how to get a mortgage”)

– Consider geographic SEO (target “personal finance for Americans,” “Canadian budgeting strategies”)

– Build an email list and partner with US-based financial companies

Step-by-Step Strategy: Maximizing Your Personal Finance YouTube RPM

Earning $10–$30 RPM is baseline. Exceptional creators push toward $35–$40 RPM by optimizing every variable. Here’s how.

Step 1: Choose Your Specific Subcategory (Not Just “Personal Finance”)

Broad personal finance channels underperform. Specific niches dominate. Choose one of these proven frameworks:

– Debt-specific: “Debt Payoff Strategies for Americans” (not “Personal Finance Tips”)

– Audience-specific: “Budgeting for Nurses,” “Personal Finance for Teachers,” “Investing for Beginners”

– Goal-specific: “How to Save $10K in 100 Days,” “Real Estate Investing for First-Time Buyers”

– Problem-specific: “Credit Repair Secrets,” “Side Hustle Income Ideas,” “How to Eliminate Student Loans”

Specificity attracts more intent-driven searches and higher advertiser bids. “Debt payoff” has 8,100 monthly searches. “Personal finance tips” has 450 searches. Which would you rather rank for?

Step 2: Build Three Foundational Content Pillars

Create a repeatable framework. Successful personal finance channels use three content pillars:

Pillar 1: Educational Foundation (40% of content)

– How-to videos: “How to Create a Budget in 5 Steps”

– Explainers: “What is Credit Score and Why It Matters”

– Comparisons: “Debt Snowball vs. Debt Avalanche: Which Pays Debt Faster?”

These build authority and rank in search results. They’re evergreen and generate consistent traffic long-term.

Pillar 2: Real-World Case Studies (30% of content)

– Document your own journey: “How I Paid Off $50K Debt in 18 Months”

– Interview others: “People Share Their Debt Payoff Stories”

– Before-and-after transformations: “We Helped 5 Families Cut Their Budget 40%”

Case studies drive engagement and build audience loyalty. Viewers see themselves in the stories.

Pillar 3: Trend & Current Events Content (30% of content)

– Market updates: “Stock Market Crash: What Your Portfolio Should

Advertisement